Part 1. The Ultimate Guide to Financial Freedom: 7 Proven Strategies for Building Wealth

9 minutes, 12 seconds read:

Hello, Sweet Money Readers,

I was recently invited by a local community group to give a talk about personal money management in my hometown.

The talk was supposed to last one hour. But because people had so many great questions and were so engaged, we talked for two and a half hours!

After this event, I saw how many people want to learn more about money and how it affects their everyday lives.

In response, the next Sweet Money Daily series will focus on the essentials getting back to personal finance basics.

The series title is: The Ultimate Guide to Financial Freedom: 7 Proven Strategies for Building Wealth.

Topics covered will include:

- Annuities

- Credit Scores, Credit Monitoring & Credit Freezes

- Estate Planning 101

- How to Buy Gold

- How to Set Up a Property Fraud Alert

- Identity Theft Prevention

- Investing 101

- Passive income Ideas

- Real Estate 101

- Tax Advantage Accounts

- And more

Let’s get started!

First, let’s answer the question: What is financial freedom?

Financial freedom means having sufficient income and assets to cover expenses without depending on a paycheck or actively working for money.

It’s about gaining control over your finances to the point where your money works for you, through investments, passive income streams, or strategic financial planning, so you can live on your own terms.

In simple terms, financial freedom allows you to:

- Live without financial stress: You can stop stressing over living paycheck to paycheck or dealing with unexpected financial setbacks.

- Have more choices: With your finances in order, you can decide based on what you want to do, not just what you must do to survive.

- Retire early or semi-retire: You can choose to work less or retire early, knowing you have enough to support your lifestyle without needing constant income.

Financial freedom is not just about having a big pile of money. It’s about designing a lifestyle that matches your values, whether through reducing debt, increasing savings, building investments, or creating sources of income that don’t require constant active work.

While financial freedom isn’t new, achieving it has become more realistic for many people in recent years.

Six Reasons Why Financial Freedom is Achievable

1. Access to Information:

Traditionally, financial advice was available only to the wealthy or individuals with expert knowledge. Today, the internet has made financial education more accessible than ever. We can find free resources, blogs, courses, podcasts, and videos that explain everything from budgeting to investing in simple, easy-to-understand terms.

Social media and personal finance blogs have become vibrant communities where individuals exchange their experiences and strategies for reaching financial freedom. This means people can learn from others successes and mistakes.

2. Affordable Investment Options:

In earlier generations, investing in the stock market or real estate often required significant upfront capital or access to expensive brokerage services. Today, low-cost investment platforms (like robo-advisors and fractional share investing) allow almost anyone with even a tiny amount of money to start investing.

The rise of index funds and ETFs (Exchange-Traded Funds) has made investing in diversified portfolios much more accessible and affordable, meaning that even people with modest incomes can steadily grow their wealth over time.

3. Automation & Financial Tools:

Financial automation has been a game-changer. Apps like Mint for budgeting, Acorns for rounding up purchases, and investing in change help individuals manage their finances without needing to manage every detail manually.

With automated savings plans and investing tools, you can set up regular deposits into retirement accounts, index funds, or other investment vehicles.

This makes it easier to consistently save and invest without thinking about it.

4. New Income Streams:

With the rise of the gig economy and online business opportunities, earning money outside a traditional job is easier than ever.

From freelancing and consulting to launching an online store or investing in real estate, there are endless opportunities to earn income without depending on a traditional 9-to-5 job.

According to a Bankrate report, more than a third of U.S. adults and nearly half of millennials and Gen Z have a second income stream.

People diversify their income sources, creating passive income streams, such as rental properties, royalties from digital content, or dividend-paying stocks.

This can reduce reliance on active work and move people closer to financial freedom.

5. Changing Social Norms:

There’s a shift in mindset, with people prioritizing financial independence and early retirement (FIRE) over traditional career paths.

This cultural change has led to a greater focus on minimizing expenses, maximizing savings, and investing wisely to retire early or semi-retire.

More people are starting to understand that living below their means, being frugal, and consciously managing money can lead to greater freedom in the long run. It’s no longer about spending for enjoyment but creating a life of intentional financial choices.

6. Increased Focus on Financial Literacy:

There’s a growing recognition of the importance of financial literacy.

People realize that managing personal finances effectively is a skill that can be learned, and the earlier it’s learned, the better.

From high school students learning about budgeting to adults enrolling in personal finance courses, the public is becoming more knowledgeable about managing money.

With this information, let’s cover Step 1 of achieving financial freedom:

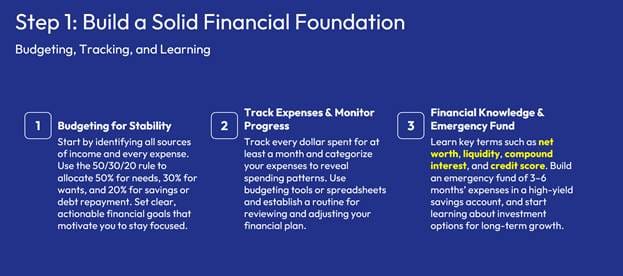

Building a Solid Foundation

Building a solid foundation in budgeting, tracking expenses, and understanding personal finance is crucial for long-term financial success.

Here are three vital measures a person can take today to strengthen their financial foundation in each area:

#1- Budgeting for Stability. We must have a firm foundation in our financial life.

A budget helps you plan your finances, allocate your income, and stay on track with savings and spending.

First, identify Your Income and Expenses.

- Action: Write down all your sources of income (salary, freelance, side hustle, etc.) and all your fixed and variable monthly expenses (rent/mortgage, utilities, groceries, etc.).

- Why: This helps you understand where your money is coming from and where it’s going. It’s the first step in gaining control over your finances.

Then you want to use the 50/30/20 Rule.

- Action: Break down your budget into three categories:

- 50% for Needs (e.g., housing, utilities, food, transportation)

- 30% for Wants (e.g., entertainment, dining out, travel)

- 20% for Savings and Debt Repayment (e.g., emergency fund, retirement, credit card payments)

- Why: The 50/30/20 Rule offers a simple and effective way to ensure you cover your essentials, enjoy life, and build savings or pay off debt.

Lastly, budgeting for stability means you want to set clear financial goals.

- Action: Set short-term financial goals (like building an emergency fund) and long-term goals (like retirement savings) and allocate specific amounts in your budget.

- Why is this important? Having goals gives you direction and motivation to stick to your budget, helping you focus on achieving financial success.

#2 – Tracking Expenses & Monitor Progress

Tracking your expenses allows you to see where your money is going and identify areas for improvement.

First, Track Every Expense for One Month

- Action: Track all your spending, whether on coffee, rent, bills, or impulse buys for one whole month. Use a note app, spreadsheet, or budgeting tool like Mint, YNAB.com, which stands for: You Need A Budget, or EveryDollar to capture your purchases.

- Why: This gives you a real-time view of your spending habits, helping you spot areas where you may be overspending.

Next, Categorize Your Expenses

- Action: Group your expenses into categories like: Groceries, Entertainment, Utilities, Dining out, etc., to see where your money is going.

- Why: Categorizing expenses will help you identify areas for reduction (for example, eating out less) and areas for reallocating funds to savings or paying off debt.

Then, Create a System for Monitoring Ongoing Expenses

- Action: Set up a monthly review process. Use a budgeting app or spreadsheet to track and categorize your monthly expenses.

- Why: This keeps you on top of your finances, allowing you to adjust as needed and avoid surprises when bills come due.

#3 – Financial Knowledge & Emergency Fund

A solid understanding of personal finance includes knowing the basics of saving, investing, debt management, and building wealth.

First, learn the Basics of Financial Terminology.

- Action: Start by learning key personal finance terms like net worth (can anyone give me the definition of net worth? It’s the value of everything you own (assets) minus everything you owe (liabilities)

- Liquidity (a persons ability to meet their short-term obligations using readily convertible assets into cash)

- Compound interest (think of it as interest on interest, where the interest earned each period is added to the principal, and the next periods interest is calculated on the new, larger principal)

- A credit score is a number that represents your creditworthiness. It’s essentially a snapshot of your history of borrowing and repaying debts. Lenders use it to assess how likely you are to repay a loan. A higher score generally indicates a lower risk to lenders, potentially leading to better loan terms like lower interest rates. FICO scores typically range from 300 to 850.

Next, you’ll want to understand the Importance of an Emergency Fund.

- Action: Set aside at least 3-6 months of living expenses in an easily accessible savings account (e.g., a high-yield savings account).

- Why: An emergency fund provides financial security in case of unexpected expenses (e.g., job loss, medical bills) and prevents you from relying on credit cards or loans.

Then, it’s good to Get Familiar with Basic Investment Concepts.

- Action: Learn the basics of investing, such as the difference between stocks, bonds, and mutual funds. Consider starting with low-cost index funds or ETFs to get your feet wet.

- Why: Investing is essential for building long-term wealth and understanding how to grow your money through smart investments can help you achieve financial freedom.

In Summary:

- Budgeting: Create a budget by identifying income and expenses, following the 50/30/20 Rule, and setting financial goals.

- Tracking Expenses: Track all your expenses for one month, categorize them, and review them regularly to identify areas for improvement.

- Understanding Personal Finance: Learn basic financial terms, prioritize building an emergency fund, and educate yourself on basic investing principles.

Today’s steps will lay the groundwork for achieving financial stability, reducing debt, and building wealth over time.

Before signing off, here’s a simple and practical budget template anyone can use to track expenses.

It includes common income and expense categories, making it easy to see where your money is going.

This template can be adjusted based on your personal financial situation.

Get Started Today with Your Personal Budget Template

Income

| Source | Amount |

| Salary | $ |

| Side Income | $ |

| Other Income | $ |

| Total Income | $ |

Fixed Expenses (These are regular, predictable costs)

| Category | Amount |

| Rent/Mortgage | $ |

| Utilities (Gas, Water, Electric) | $ |

| Internet/Phone | $ |

| Insurance (Health, Auto, Life, etc.) | $ |

| Car Payment | $ |

| Student Loan | $ |

| Subscriptions (Netflix, Gym, etc.) | $ |

| Total Fixed Expenses | $ |

Variable Expenses (These are flexible and may change month-to-month)

| Category | Amount |

| Groceries | $ |

| Transportation (Gas, Bus, Uber) | $ |

| Dining Out | $ |

| Entertainment | $ |

| Clothing | $ |

| Personal Care | $ |

| Medical (prescriptions, doctor visits) | $ |

| Other | $ |

| Total Variable Expenses | $ |

Savings & Investments (These should be prioritized for future financial growth)

| Category | Amount |

| Emergency Fund | $ |

| Retirement (401k, IRA, etc.) | $ |

| Short-Term Savings (Vacation, Big Purchase) | $ |

| Investments | $ |

| Total Savings/Investments | $ |

Debt Repayment (Paying down debts beyond just minimum payments)

| Category | Amount |

| Credit Card Debt | $ |

| Personal Loan | $ |

| Other Debt | $ |

| Total Debt Repayment | $ |

Total Overview

| Category | Amount |

| Total Income | $ |

| Total Fixed Expenses | $ |

| Total Variable Expenses | $ |

| Total Savings/Investments | $ |

| Total Debt Repayment | $ |

Net Income/Surplus/Deficit

| Calculation | Amount |

| Total Income – Total Expenses | $ |

How to Use This Template:

- Track Your Income: Write down all your sources of income each month. This could include your regular salary, side jobs, or passive income streams.

- Log Fixed Expenses: Fill in your fixed costs, such as rent, mortgage, insurance, and any other monthly commitments that stay the same. These are your non-negotiables.

- Track Variable Expenses: These are costs that fluctuate every month, like groceries, transportation, and dining out. Monitor these carefully and adjust where it is possible to stay within budget.

- Add Savings and Investments: Ensure you contribute to savings and retirement accounts. Even small contributions can help build a strong financial foundation.

- Debt Repayment: First, focus on paying off high-interest debts (like credit cards) and allocate money to reduce your monthly debt.

- Net Income: At the end of the month, subtract your total expenses from your total income. If you have a surplus, that’s great to put that extra toward savings or investments. If you have a deficit, identify areas where you can cut back.

Tips for Staying on Track:

- Automate Payments: Set up automatic payments for fixed expenses like rent, utilities, and savings. This can reduce the temptation to overspend.

- Cut Back on Non-Essentials: If you’re spending too much on things like dining out or entertainment, look for ways to reduce these costs and reallocate the savings to debt or investments.

- Review Regularly: Check your budget monthly to see where your money goes. Adjust as needed.

That’s it for this today.

Until next time, keep investing!

Disclaimer: We will not track any recommendations in Sweet Money Daily. We are just sharing our opinions, not advice. If you want access to the stocks in our model portfolio with tracking, updates, and buy/sell guidance, please check out The GenWealth Report.

{kind=link}